Is Financial Leasing the Most Efficient Alternative for Business Financing?

Is Financial Leasing the Most Efficient Alternative for Business Financing?

By: Juan Bautista López

For the optimal performance of companies, investing in capital assets such as machinery, equipment, and vehicles is essential. These assets enable the economic exploitation of operations, improve service quality, optimize production processes, and, in some cases, reasonably reduce labor costs.

Such investments must be made after carefully evaluating the most convenient financing alternative to avoid undermining the company’s financial health, mitigate risks, reduce financial costs, and maximize tax benefits. In this context, the following question arises: Is financial leasing the most efficient alternative for business financing?

Definition of Financial Leasing

Douglas R. Emery, in his book “Fundamentals of Financial Management”, provides a concise description of financial leasing and its benefits:

“Financial leasing represents an important source of long-term financing. Entering into a financial lease is similar to signing a loan agreement, since the company obtains the same economic benefits it would receive if it had purchased the asset, excluding the tax effects”.

Companies widely use financial leasing to acquire capital assets when they lack sufficient liquidity to fund an immediate purchase. In Peru, this mechanism is regulated by Legislative Decree No. 299.

In a financial leasing contract, three parties are involved:

- The supplier or manufacturer of the asset, who sells the asset.

- The financial entity (i.e., the lessor), which acquires the asset and finances 100% of its value.

- The lessee (i.e., the user company), which uses the asset and pays periodic installments over the term of the contract.

The widespread use of financial leasing is mainly attributable to two factors: competition among financial entities, which has reduced interest rates, and, more importantly, the tax benefits associated with this modality.

Tax Advantages of Financial Leasing

1. VAT Treatment

One of the main advantages of financial leasing is the deferral of Value-Added Tax (VAT). Unlike a direct purchase, where VAT is paid in full at the outset, under a leasing contract this tax is paid proportionally with each installment, generating monthly VAT credits and improving the company’s cash flow.

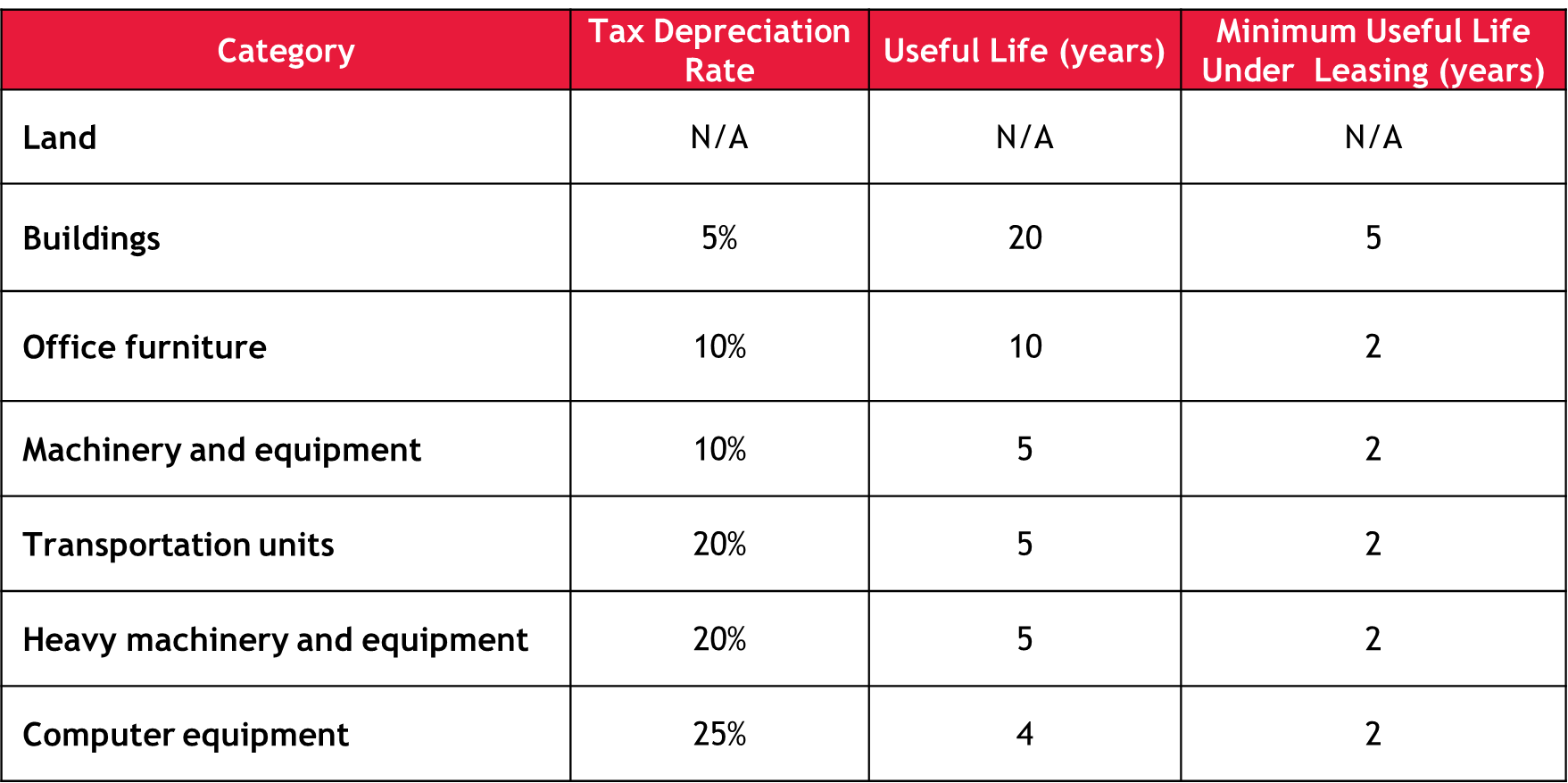

2. Accelerated Depreciation

Another significant benefit is the accelerated depreciation of the leased asset over the term of the leasing contract. This allows the value of the asset to be recognized as a deductible expense for income tax purposes over a shorter period than its normal useful life.

Below is a comparative summary of tax depreciation rates and the minimum terms applicable to financial leasing contracts:

For these reasons, many tax specialists recommend financial leasing as a tax planning tool aimed at reducing the taxable base for income tax purposes while ensuring compliance with applicable regulations.

Disadvantages of Financial Leasing

Despite its significant advantages, financial leasing also presents certain disadvantages that should be considered in business decision-making:

- Legal ownership of the asset is transferred to the lessee only upon exercising the purchase option at the end of the contract.

- Any modification, improvement, or adaptation of the asset requires prior authorization from the financial entity, which remains the legal owner throughout the term of the contract.

- In many cases, prepayments or early termination are subject to penalties. In addition, if the contract is terminated before the minimum statutory term (24 months for movable assets and 60 months for real estate), the benefit of accelerated depreciation is lost.

- The lessee is responsible for the maintenance of the asset. If the asset becomes obsolete or the project is no longer profitable, there is no option to return it.

Position of Business Associations and Financial Institutions

The Association of Banks of Peru (ASBANC) states that financial leasing is an ally of productive activities, as it reduces the need for initial cash outlays, optimizes financing costs, and allows taxpayers to benefit from accelerated depreciation for income tax purposes.

Furthermore, various financial entities actively promote leasing among business associations, particularly within the medium-sized enterprise segment, highlighting its positive impact on cash flow and tax burdens.

Conclusions

Before investing in capital assets, each company must perform a comprehensive evaluation to determine whether a traditional loan or a financial leasing arrangement is more convenient. From a professional standpoint, financial leasing is often a highly efficient alternative, primarily due to its tax benefits and its favorable impact on liquidity.

However, management must be aware that every financing decision entails risk. Accordingly, the choice between leasing, borrowing, or using own resources should be supported by a prior analysis of projected cash flows, considering both explicit and implicit costs, as well as the interest and obligations assumed throughout the financing period.

In summary, financial leasing should not be considered solely based on its interest rate, but rather on its total financing cost and its long-term tax and financial impact.